I’ve long advocated that anyone who expects to live a long life should consider deferring their Canada Pension Plan to age 70. Doing so can increase your CPP payments by nearly 50% – an income stream that is both inflation-protected and payable for life. If taking CPP at 70 is such a good idea, why not also defer OAS to age 70?

Many people are unaware of the option to defer taking OAS benefits up to age 70. This measure was introduced for those who retired on or after July 1, 2013 – so it is still relatively new. Similar to deferring CPP, the start date for your OAS pension can be deferred up to five years with the pension payable increased by 0.6% for each month that the pension is deferred.

OAS Eligibility

By the way, unlike CPP there is no complicated formula to determine your eligibility and payment amount. That’s because OAS benefits are paid for out of general tax revenues of the Government of Canada. You do not pay into it directly. In fact, you can receive OAS even if you’ve never worked or if you are still working.

Simply put, you may qualify for a full OAS pension if you resided in Canada for at least 40 years after turning 18 (when you turn 65).

To be eligible for any OAS benefits you must:

- be 65 years old or older

- be a Canadian citizen or a legal resident at the time your OAS pension application is approved, and

- have resided in Canada for at least 10 years since the age of 18

You can apply for Old Age Security up to 11 months before you want your OAS pension to start.

Your deferred OAS payments will start on the date you indicate in writing on your Application for the Old Age Security Pension and the Guaranteed Income Supplement.

There is no financial advantage to defer your OAS pension after age 70. In fact, you risk losing benefits. If you’re over the age of 70 and not collecting OAS benefits make sure to apply for OAS right away.

Here are three reasons why you should defer OAS to age 70:

1). Enhanced Benefit – Defer OAS to 70 and get 36% more!

The standard age to take your OAS pension is 65. Unlike CPP, there is no option to take OAS early, such as at age 60. But you can defer it up to 60 months (five years) in exchange for an enhanced benefit.

Deferring OAS to age 70 can be a wise decision. You’ll receive 7.2% more each year that you delay taking OAS (up to a maximum of 36% more if you take OAS at age 70). Note that there is no incentive to delay taking OAS after age 70.

Here’s an example. The maximum monthly payment one can receive at age 65 (as of 2024) is $713.34. Expressed in annual terms, that equals $8,560.08.

Let’s look at the impact of deferring OAS to age 70. Benefits will increase by 0.6% for each month of deferral, so by age 70 we’ll see a total increase of 36%. That brings our annual OAS pension to $11,641.71 – an increase of $3,081.63 per year for your lifetime (indexed to inflation).

2). Avoid / Reduce OAS Clawback

In my experience working with clients in my fee-only practice, retirees are loath to give up any of their OAS benefits due to OAS clawbacks. That means designing retirement income and withdrawal strategies specifically to avoid or reduce the OAS clawback.

The Canada Revenue Agency (CRA) calls this OAS clawback an OAS pension recovery tax. If your income exceeds $86,912 (2023) then the OAS recovery tax will claw back your OAS payments in the period between July 2024 and June 2025. For every dollar of income above the threshold, your OAS pension is reduced by 15 cents. OAS is fully clawed back when income exceeds $142,124 (2023).

So, does deferring OAS help avoid or reduce the OAS clawback? In many cases, yes.

One example I’ve come across many times is when a client works beyond their 65th birthday. In this case, they may want to postpone OAS simply because they’re still working and don’t need the income. In some cases, the additional income received from OAS would be partially or completely clawed back due to a high income. Deferring OAS to at least the next calendar year when you’re in a lower tax bracket makes a lot of sense.

Aaron Hector, financial consultant at Doherty & Bryant, says there is a clear advantage to postponing OAS if someone expects their retirement income to push them into the OAS clawback zone.

“Not only will postponement provide them with an enhanced OAS income, it will also in turn provide them with a higher clawback ceiling,” said Mr. Hector.

It might also allow the opportunity to draw down RRSP/RRIF assets between 65 and 70 which would reduce future expected retirement income (lower RRSP/RRIF assets = lower mandatory withdrawals between age 72 and death).

One could also stash any unspent RRSP/RRIF withdrawals into their TFSA. Growing their TFSA in retirement gives retirees the valuable ability to withdraw money tax-free any time and not have that income affect their means-tested benefits (such as OAS).

3). Take OAS at 70 to Protect Against Longevity Risk

It’s counterintuitive to defer taking pensions such as CPP and OAS (even with an enhanced benefit for waiting) because it forces retirees to tap into their personal savings – depleting their nest egg earlier and faster than they’d prefer. Indeed, people are reluctant to spend their capital.

But this is a good thing, according to Retirement Income For Life author Fred Vettese. Deferring CPP and OAS increases the amount of guaranteed income you will have for the rest of your life, while also reducing your long-term investment risk because you are spending your savings first.

“Spend your risky dollars first because they may not be there for you in your 80s, depending on how your investments do. A bigger CPP (or OAS) cheque, however, will definitely be there for you.”

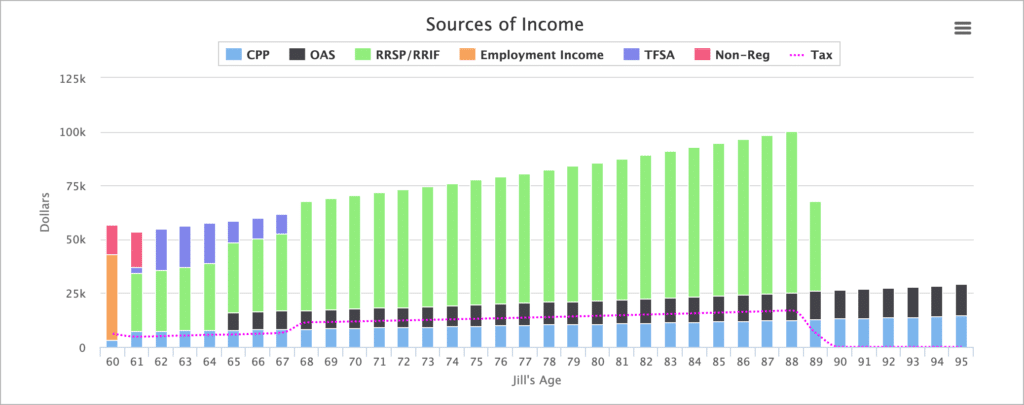

In one example I looked at a single 59-year-old woman – Jill Smith – who plans to retire on July 1st when she turns 60. Jill requires $48,000 in after-tax spending each year to meet her retirement goals.

She has $775,000 saved in her RRSP, plus $75,000 in her TFSA and $30,000 in cash. She’ll qualify for 80% of the CPP maximum and is fully eligible for OAS.

If Jill takes CPP right away (July 2) at age 60 and takes OAS at the standard age 65 she’ll have enough personal savings to last until she’s 89. Her CPP and OAS pensions make up 30.39% of her total annual income in retirement.

Now let’s compare this scenario with deferring CPP and OAS to age 70.

Not only does Jill increase the viability of her retirement plan – her personal savings now last until age 92 – but she has increased the portion of index-protected, paid-for-life government pensions to 54.25% of her total annual income.

Mr. Hector says that someone who fears running out of money in old age would be wise to postpone OAS to guarantee a higher base level of income when they are very old.

So those are three great reasons to take OAS at 70 – to enhance your annual OAS benefit, to reduce or avoid OAS clawbacks, and to protect against longevity risk.

Now let’s look at four reasons why you might not want to defer your OAS pension past 65.

1). The OAS Enhancement Is Less Enticing Than CPP

The actuarial adjustment you receive for deferring OAS to age 70 is much less than it is for deferred CPP to 70. It is just 36% compared to 42% for CPP. That makes a big difference, considering you’re foregoing your pension for five years. You want to make sure it’s worthwhile.

“When I compare the two side by side it really jumps out at you how there is a much greater incentive to deferring CPP than there is to defer OAS. This of course is due to the fact that there is a greater enhancement effect for CPP,” says Mr. Hector.

Ignoring income and clawback concerns, it is best to take OAS at age 65 for someone who is going to die between 65 and 79 for OAS, but for CPP the range shrinks to 65 to 77.

Taking OAS at age 70 gives the best outcome for those who live to age 88 and beyond.

2). Emotional Factor

Fred Vettese is a big proponent of deferring CPP until age 70 but not as enthusiastic about deferring OAS. He says that starting CPP late is already forcing the average retiree to draw down their RRIF balance much faster than they planned on doing. It is still a good move, but one that makes people uncomfortable.

He says asking people to start OAS late as well will accelerate the RRIF drawdown and make people that much more uncomfortable.

3). You Need The Money

Deferring CPP and/or OAS is a luxury for those who have the means to fund their lifestyle while they wait. Repeat: This is not a strategy for those who need to access their government benefits right away to get by.

Mr. Vettese says you need at least $200,000 saved before even considering the deferral strategy.

4). Leaving an Inheritance

Deferring OAS and CPP until age 70 means spending down a good portion of your personal savings in your 60s. This could also mean it’s possible to spend down most if not all of your personal savings before you die.

Related: The Retirement Risk Zone

While this ‘die broke’ strategy may be ideal for some, others may wish to leave an inheritance to their loved ones or to charity.

As there is no survivor-OAS pension, someone who is concerned about leaving a large estate to their heirs may decide that they would rather take OAS earlier so that they can leave their investments intact.

“The investments will always have a value for their beneficiaries but that is not true for someone who opted to defer OAS,” says Mr. Hector.

Final Thoughts

There’s no clear-cut answer for deciding if and when to defer OAS.

When I’m working with clients, I always make sure they understand to at least postpone taking OAS until retirement, or the next calendar year after retirement to avoid OAS clawbacks and additional taxes in the final working year.

Then we look at OAS clawback amounts (if any) and see what can be done to avoid them. Sometimes that means taking more from their RRSP/RRIF in their 60s while deferring OAS until somewhere between ages 67 to 70.

But the bottom line is that deferring OAS to 70 is a bet that you’ll live a long life. And, like with an annuity, rather than worrying about what happens if we die early, we should give more thought to whether we’ll live longer than expected.

With that in mind, deferring OAS by 1-5 years can help transfer the risk from your personal savings to the inflation-protected, paid-for-life government pension program.

The more we can ‘pensionize’ our retirement income, the better off we’ll be if we happen to live an extraordinary long life.